Advertisement

QOTW: Catch-ups

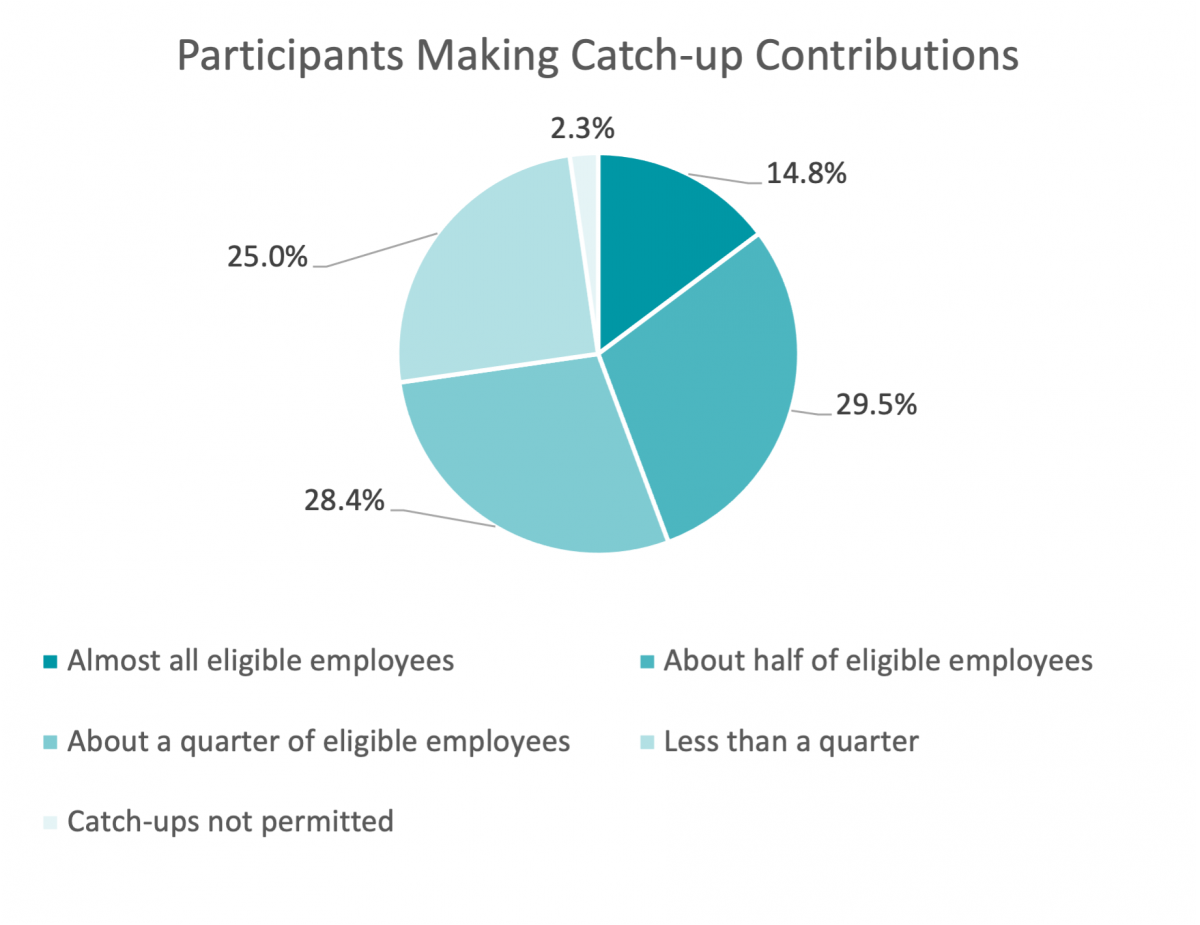

A provision in the EARN bill in the Senate included a requirement for catch-up contributions to be Roth after-tax contributions (as a pay-for for other provisions). We wondered how much participants actually use the catchup provisions and what impact a Roth requirement would have. Thirty percent of respondents indicated that about half of eligible employees make catch-up contributions, 15 percent stated that most all do, and more than half stated a quarter or fewer participants make catchups. Fewer than a quarter of plan sponsors provide targeted education around catch-up contributions.

More than a third of respondents stated that requiring catchups to be Roth would impact participants, yet nearly half were not sure. The comments seemed split on this – some say that participants only make them for the tax benefit so would stop if forced into Roth, whereas others stated only HCEs make catch-ups or that most of their employees can’t afford to make catchups anyway so it’s a non-issue. Read more below.

- 5 of 111 eligible participants are utilizing catch-up contributions. All contributions are currently pre-tax.

- Any restrictions we place on catch-ups I believe would have a negative impact. We can continue to emphasize in group/individual employee meetings the opportunity to maximize contributions via catch-ups.

- Catch-up is automatic within our plan, rather than elected. Meaning once eligible participant reaches 402g limit, catch-up commences automatically for those age 50+.

- Catch-ups are out of reach for all but the very highest paid employees. For us, it’s the owner and one vice president with significant outside financial resources. Only the wealthy can take advantage.

- Catch-ups are used by all eligible executives and most other HCEs, but it’s rare for a non-HCE.

- Depending on participants financial position, requiring catch-ups on Roth contributions could cause negative impact for participants, as they may not be able to afford the additional catch-ups.

- hard to measure catch up participation / usage since catch up contributions are really only relevant to employees who are maximizing their core contributions – and the majority are not.

- I am thinking that it would since most of the ones utilizing the catch up is doing so for tax benefit

- I like the idea of flexibility and not forcing catch-ups to be Roth. We've elected they can be either.

- I think Roth requirements would negatively impact our company and plan.

- I'm not sure what the advantage would be to require Roth catch-ups.

- If eligible employees aren't getting to the general limit, don't think that a targeted communication that there is a catch up limit will move the mark.

- in our company generally only highly comped take advantage of catch-up contributions.

- It would be administratively difficult, but there are currently only 2 individuals utilizing catch-ups and both are contributing pre- and post- tax

- It would require education as not everyone understands or likes Roth contributions. There is also probable reprogramming of payroll to ensure all catchup were Roth.

- Most don't make enough or work enough hours to make a significant difference with the catch-up contributions in a year

- Most high contributors do so for their lifetime and may use the catch-up but they represent well less than a quarter. Persons who have not been contributing at high rates prior to qualifying for the catch-up provision rarely begin contributing at high enough rates to need the catch-up.

- Never thought about this!

- Only 1 EE makes enough to afford catch-ups.

- Only 1 participant making catch-ups is making Roth contributions in our Plan.

- Only 11% of those eligible, based on age, make catch-up contributions, but if we looked only at those who reached contribution limits, the percent may be higher. Our plan allows for regular and catch-up contributions to be made simultaneously.

- Only a couple of employees take advantage of catch-up contributions. A lot of eligible employees don't even contribute any employee amounts to their retirement plan. All employees are informed about catch-up contributions, but very few are contributing at all, let alone contributing near the annual basic IRS limit.

- Only a couple of our age-eligible employees have ever contributed the maximum annual contribution. As we are a retail industry, most of our employees are not highly paid, and a large percentage are younger. A couple of high level management people and one older (70s) person who lives frugally on SS while saving 100% of his working income has contributed enough to utilize catchup contributions.

- Our plan does not have a separate catch up election. If one is over age 50 then the plan allows for contributions up to the 402g + catch up limit automatically. Forcing the catch up to be Roth would require changes to our plan and RK system and would require people to start electing. We are not in favor of that.

- Ours is a voluntary plan, which is supplemental to a defined benefit plan. Our plan does not offer a Roth feature and has no plans to.

- Requiring catch-up contributions to be Roth would affect how many make catch-up contributions.

- Roth is great if you can afford to pass up the current tax break for a future tax break. Many cannot afford to do that. I don't think you should force Catch ups to be Roth. That should be up to the participant. Also, our Catch-up contribution is not a separate contribution. It's combined with our regular contributions.

- Roth will not be a participant’s choice for catch-up. They will fill like they are pushed to have 2 different accounts. I will hear a lot of complaints. It won’ be a popular move.

- Since our HCEs are limited to a lesser deferral contribution rate they are allowed to contribute simultaneously to catch up while our NHCEs need to hit their IRS regular deferral maximum before the catch-up contributions will start deducting.

- Unfortunately most employees are financially unable to make catch-up contributions.

- Very concerned for the impact on our recordkeeping and payroll systems for mandatory Roth treatment of catch-up contributions, and the need for re-education of our participants.

- We allow 50+ participants to elect regular and catch-up so they're contributing to these at the same time.

- We are a small company with only 15 employees/participants. Typically, it's the higher earners that take advantage of the catch-up option.

- We don't require a separate enrollment or authorization for catch-ups, so if someone's chosen contribution percentage will attain the base annual limit, and beyond, we don't necessarily know about it.

- We have a very young staff who do not qualify for catch-ups yet.

- We offer pre-tax and Roth catch-up contributions. Most of the highly compensated employees make catch-up contributions.

- Would not see the participation. Those employees looking for the tax break now and not later.