Advertisement

QOTW: EARN Provision

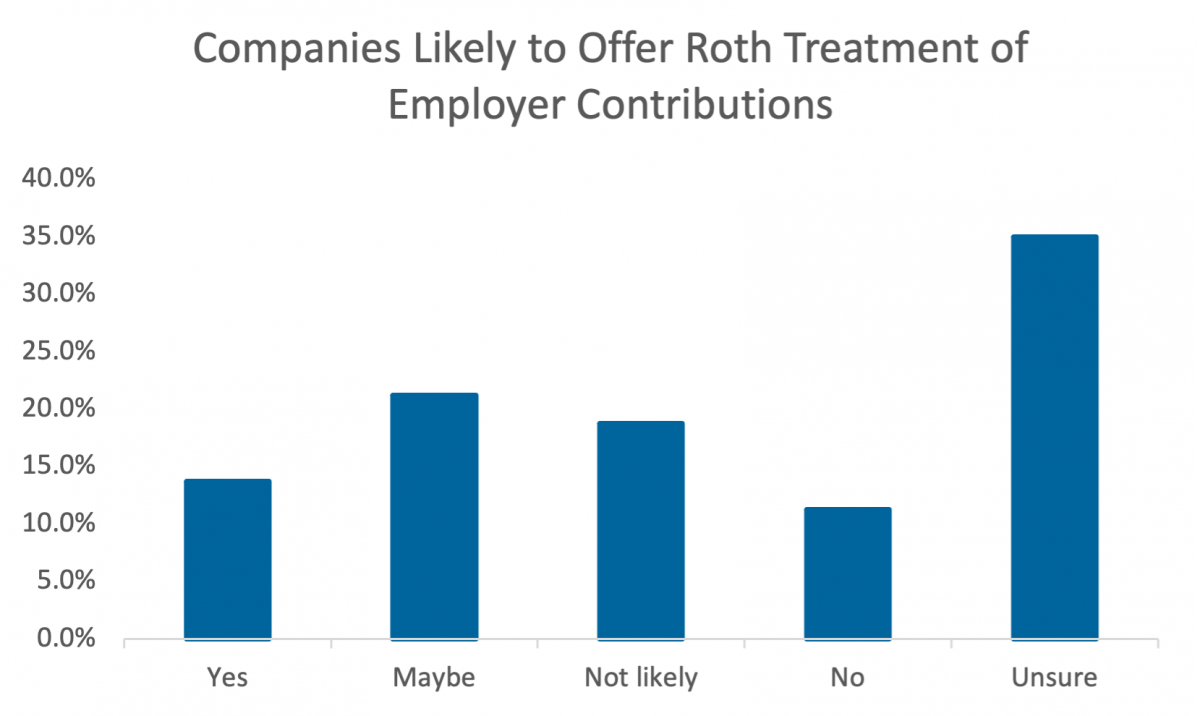

One of the revenue-raising provisions currently in the EARN (Enhancing American Retirement Now) Act that was passed out of committee in the Senate last month, is a provision that would permit an employee to elect to treat employer matching and other employer contributions as after-tax Roth contributions. This week we asked members if their company was likely to adopt such a provision. Only 14 percent of companies said they would, with 21 percent saying maybe. The comments on this span from it’s a great idea to no way – the main concern seems to be the additional administrative burden in implementing such a provision.

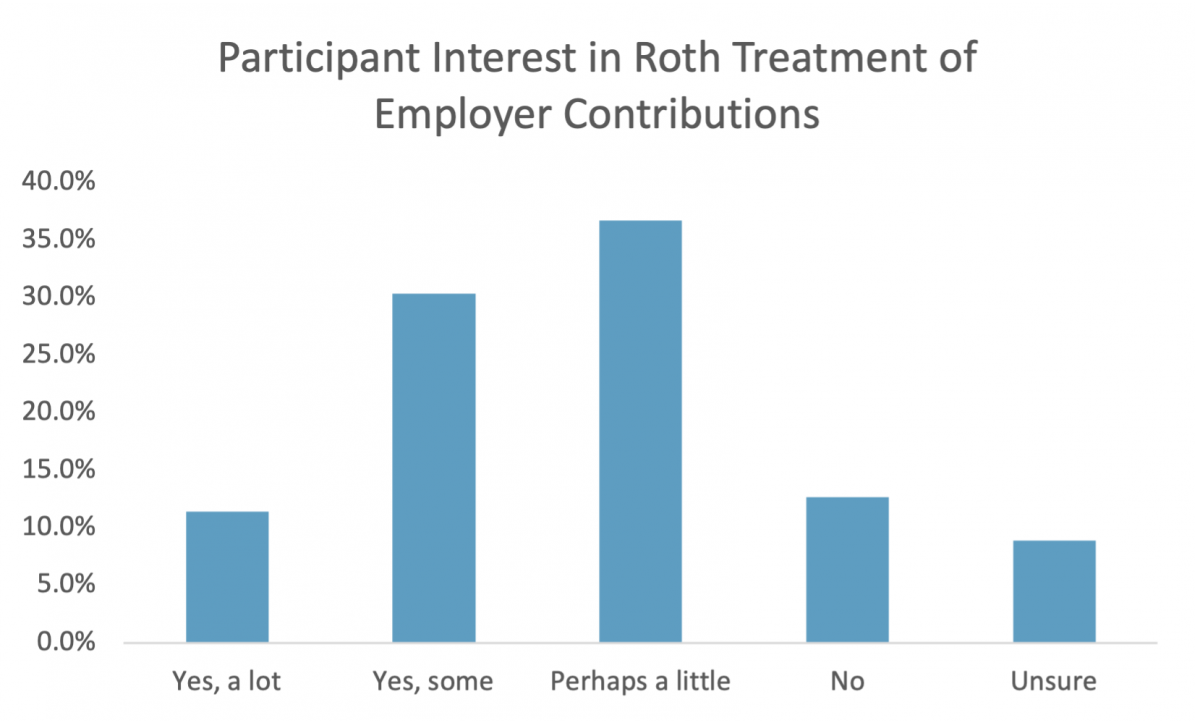

We also asked members if they thought there would be much participant interest in treating employer contributions as Roth contributions. Eleven percent said there would be a lot of interest with 30 percent indicating they thought there would be some interest and another 37 percent stating “perhaps a little.”

Comments follow.

- Absolutely love it for participants - give them choice! Administratively, it would add work as those choosing Roth would need taxed on the match but no issue absorbing that work for the benefit of participants.

- Areas of concern are the payroll system and the W-2. I assume that this benefit will be added to compensation.

- As a non-profit organization, there is a minimum savings rate among employees.

- Employees already have the option to elect pre-tax or Roth contributions.

- Every year we get more people turning to Roth contributions, I expect the trend to continue for some time.

- Extra issue on taxation to the employee, which may not be the positive that it's intended.

- I am not sure how this would play out.

- I assume that the employee is paying the taxes, correct?

- I would have to see the provision. Would the contribution be treated as taxable to the employee in the year of contribution?

- If it assumed to be after tax, that means the employer would have to pay the tax for the employee. If that is the case, it is unlikely we would do so. If we didn't have to pay the tax, we would be interested.

- In general, we are not early adopters. We'd ideally evaluate the experience of others and make a later determination on our course of action.

- It is not under consideration.

- It will depend on recordkeeper programming and our payroll resources. Not sure we will do this.

- Not a strong appetite currently, but willing to learn more.

- Only really savvy participants might be able to appreciate the benefit to incurring a current taxable event on employer contributions. If we were to ever implement it, I would want to set it up as optional, which would be an extra administrative burden. We barely have employees elect ROTH on their own.

- Our current plan only offers pre tax employee contribution. It would be interesting to see how much work would be involved in offering and maintaining an after tax option.

- Our governmental plan doesn't have a Roth option.

- Our Plan is pre-tax contributions only. We do not have a Roth option in our Plan.

- Participation would likely be those currently interested in Roth contributions. However, we make this contribution in a lump sum once a year, it could result in a tax surprise that some participants may not be prepared for.

- Revenue raising on the back of employees' retirement. Terrible

- The company gets a tax benefit from the dollars used to match employee contributions, and changing them to an after-tax basis would revoke that benefit and make this a capital budgeting decision. Thinking toward the future, it seems that this could have a negative effect on plan participants – employers wanting to offer a new plan would lose some incentive to offer a more generous match or non-elective formula without the tax break. If this is made mandatory, given anti-cutback rules, will an exception be made for a formula change if an employer has depended on those tax breaks to make their overall budget work and now find themselves unable to afford the promised match/non-elective contribution due to the additional tax burden? If it is not made mandatory, would employers find themselves with a morale issue among employees who wonder why their own company is not offering this benefit (creates a messaging problem to employees who think their company is just being greedy when in actuality it may not be affordable)? I believe this would be quite popular with employees; after all, why would an employee not want their match and non-elective contributions to grow tax-free? The reason people choose pre-tax contributions out of their own pay is to lower their AGI - since this doesn't affect their own tax situation, I cannot think of a single reason why they wouldn't take advantage. Bottom line for me is that I'm torn on the issue. As an employee I want to take advantage of this myself, but as an administrator I can also see how it could be a nightmare for employers to navigate the nuances of finance and messaging in a way that is beneficial to all involved.

- Those close to retiring who do not want to use SS until the maximum age is hit.

- Too administratively complex, can be accomplished through existing Roth conversion feature

- We already allow In Plan Roth conversions of these sources. Most of our participants are not willing or able to pay the associated taxes.

- We can designate our contributions for Roth but I am not sure if our plan allows for the Company portion to be designated as a Roth contribution. I will have to find out.

- We don't fund match through payroll, so adding the match to payroll would be prohibitive for our situation. There aren't enough details to know how this would work mechanically/administratively and that is critical to our team of 2. The take up on Roth is our plan is already low and though we allow in plan conversions but no one has done that. So, I wouldn't expect a big interest in this.

- We have not researched this option but will add it to our agenda.

- What an administrative nightmare.

- With a significant population of highly compensated attorneys, we would likely implement this provision. I’m sure it would be well received, especially with the younger population.

- Would require a Plan amendment and additional record keeping / administration. Participant use of such a feature would not be worth the cost and effort.