Advertisement

QOTW: ESG Suitability

Opinions on ESG funds are as polarized as … well as politics in this country these days. And the fact that guidance on ESG shifts depending on which political party is in the white house, it is no wonder. And, it looks like we may be getting more guidance soon.

A recent reader poll of advisors by NAPA.net showed some shift in opinions about ESG by advisors over time so we wanted to know if plan sponsors’ opinions have changed as well. We asked plan sponsors in our QOTW, not just if their company offers one, but their thoughts on suitability for a plan lineup. Most companies do not offer one, though 10 percent said they do, much higher than the 3.2 percent in our annual survey. Most comments leaned towards no, ESG funds just don’t make the cut in terms of the IPS, cite fiduciary risk, lower returns, lack of participants interest or … the fact that their company is in the field of fossil fuels or some other industry that ESG funds typically exclude.

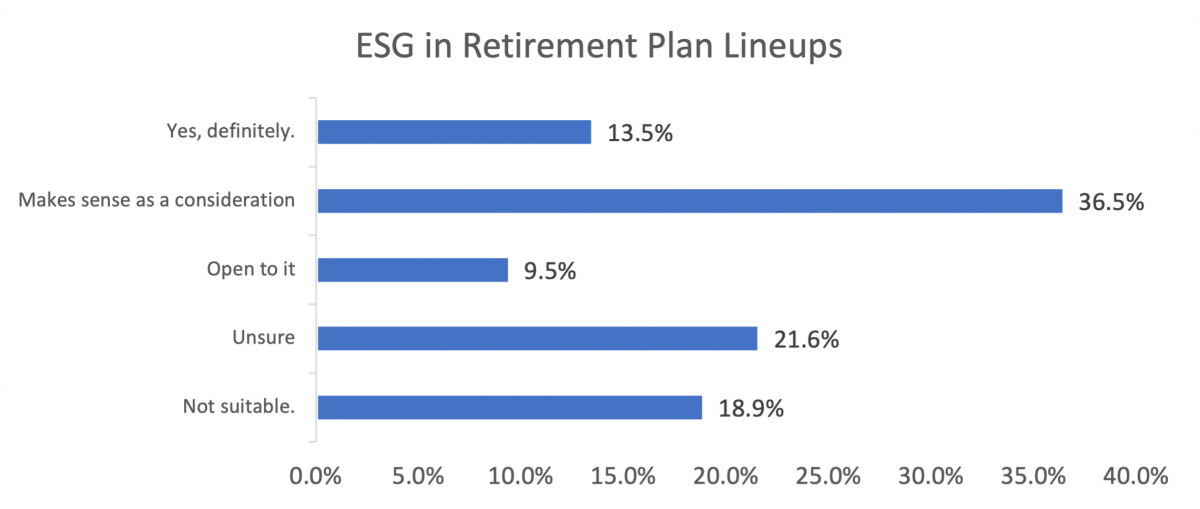

While nearly 20 percent of respondents indicated they do not think ESG is ever suitable in plans, 22 percent are unsure, and the rest are open it or think they are plan appropriate. A plurality stated that ESG makes sense as a consideration, but not a controlling one when selecting investments.

Interestingly, plan sponsor opinions on this line up reasonably well with advisor opinions with 36 percent of advisors also saying they think it makes sense as a consideration, though not a controlling one and 10% on board with the idea and 16% open to it.

Plan sponor comments follow.

Do not offer ESG:

- 1) Have not had significant volume of participant requests; 2) We have a self-directed option for participants if they do have a desire they can access ESG in that manner; and 3) vast majority of our current plan funds are directed to target date funds. Based on these factors it doesn't make sense at this time, but we will continue to monitor interest.

- Awful investment solution, especially for a 401k plan. I can't believe so much promotion is going on over ESG's.

- Employees can access those funds via our brokerage account. Also, ESG funds have higher expense ratios without necessarily a corresponding higher return. Need to have our fiduciary hat on when determining fund in the line up - i.e. best funds available.

- ESG funds don't make the cut in our Investment Policy Statement.

- ESG has many definitions depending on who you ask, the ESG mutual fund holding are the same top 10 as S&P 500 fund holdings with grossly higher costs. ESG is a farse.

- ESG is a violation of our fiduciary duty of exclusive benefit to operate the plan with exclusive purpose of providing benefits to participants and beneficiaries. Environmental-is the climate changing? Maybe, but drastic changes at significant costs on account of what may be a 100 year issue does not make sense. Social-a further dividing of the country and companies into select groups will have drastic effects. Governance-added costs for rules that are already in place. The better question is should plans consider removing funds, like BlackRock, that are pushing their own agenda and ignoring plan sponsor's fiduciary duty to operate their plans at the exclusive benefit of the plan participants.

- Executives are backing away from ESG as recession risks mount - Bloomberg Report. If executives are backing away then how can it be a fiduciary item for a fund in a 401K plan. Need to have best funds for participants.

- Fiduciary concerns

- Fiduciary Risk

- For the same reason we don't insist that we have funds that start with every letter of the alphabet. Funds should be selected on returns/risk/fees and not some arbitrary measure subject to manipulation.

- Higher fees for less performance

- I am not responsible for choosing the Plan's funds, but I personally believe that only pecuniary factors should be considered in the selection of funds.

- I believe ESG is another money grab just like climate change.

- I know some of my employees would prefer that choice regardless of returns, but I'm not sure all employees would be able to weigh the pros and cons.

- I think ESG is misleading - they're not 100% divesting from the stuff you would think but people don't understand that. That said, if one wants to invest in a company that's env conscious, that's fine.

- I think they will increase in popularity, especially as the younger crowd gets serious about retirement. It's worth the investment committee having a conversation and keeping it as an agenda item on the back burner.

- Investment committee is not comfortable with adding them.

- Investments in a 401k plan should have financial goals to build retirement savings, not push someone else's political agenda.

- It's hard to find a common cause that would please everyone. We offer a brokerage window and our participants are welcome to invest outside of the core investment lineup.

- Looking into it and the funds would need to qualify based on historical performance. Likely it would be an additional fund, not a replacement and for a cause that is applicable to our business.

- No need/requests.

- Not a priority of the decision maker

- Not compatible with our industry

- Not in our investment policy

- Our 3(38) advisor hasn't recommended it yet.

- Our company operates convivence stores and sells gas, diesel, propane and other fossil fuels.

- Our offerings include target dated funds and categories like small cap, large cap and bond funds. We offer a self-directed brokerage account for those wanting to invest in additional offerings. ESG is viewed as a specialty category like precious metals or industry specific funds.

- our primary focus should be on the health of the participant's account, not politics

- Participants have varying sensitivities to what they consider suitable in the ESG arena. Too difficult to manage the underlying investments in ESG funds to that end.

- regulatory questions at this point. once that gets some direction, I think we would be more comfortable considering adding one to our plan.

- Strongly considering but the offerings need to be widened a bit

- Too many competing interests

- We did offer one briefly, but it was expensive and uptake was not great. Cost and performance must be considered, and employees must be educated. Even if uptake is low, I think it is a valuable to offer good ESG funds. Costs have come down, there are more options now, and if you want to attract savvy employees, and telegraph that you know what is going on in the world and care about it, this is an easy way to do something.

- We have not brought it to the table for the investment committee to consider. Do plan to discuss early in 2023.

- We're waiting on further guidance from the DOL before adding.

- We've explored the possibility, but the economics (poor performance) overall haven't been satisfactory to consider.

Offer ESG in the plan:

- As a MEP plan sponsor, we added an ESG fund to our lineup at the request of several of our adopting employers.

- Participant demand--as one of many diverse offerings.

- Some people, the younger generation especially, are concerned about environment, government regulations, etc. and would like to know the money they have invested is not being utilized to support companies they don't want to support.

- We offered one for diversity in our plan offerings and to encourage younger employees to contribute to the plan but we have seen little interest from staff in investing in the ESG fund so we are removing it from our investment menu.